SETTING UP A STRATEGIC INFORMATION UNIT

Ruth Stanat suggests undertaking a strategic information audit, to evaluate what is being provided at present compared with the real needs of the organisation. The audit would also cover the effectiveness of current information sources, and of the means by which information is distributed within the organisation. Here we will choose to treat industry and competitor analysis as a separate subject, any strategic information system should cover these needs as well as those arising from the broader environment.

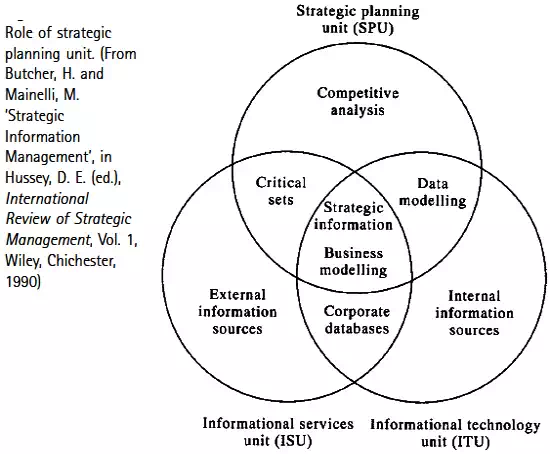

From the above figure by Butcher and Mainelli, relates the role of an external information unit, to information systems and strategic planning units. A key aspect is being aware of the interfaces where more than one of the units has both a need and a responsibility. Successful strategic information management involves managing these to avoid duplication, and making sure that the responsibilities of all three are considered. Butcher and Mainelli divide information into three types:

Information for assumptions: tends to be trend information for stable assumptions, e.g. average customer size, and discrete events for unstable assumptions, e.g. an assumption of new entrants in a market would be contradicted by news of a major acquisition of a competitor. Information for decisions: on a strategic level, the information tends to be voluminous and oriented to specific new projects or cancellations.

Information for success factors: measurement tends to be exact for internally supplied information, but base statistical information may be all that is available for external information, e.g. a success factor of press coverage could be measured by column inches multiplied by impact factor of publication. We will look more closly at information requirements for competitor analysis, and ways of compressing information so that management can track the important issues, in later chapters, including a case history which deals with both the task of obtaining relevant information in a legal and moral way, and the tracking problem.

In this chapter we will next look at ways of determining what issues are relevant to the strategic management of a particular organisation. There are similarities in a number of the methods available, and many of them seem to have been developed around the same time, in the mid-to late 1970s. We will discus two methods in some detail, one by David Hussey’s consultiong organisation and other by Fred Neubauer, Lausanne. And also some of the similar approaches, for example Hargreaves and Dauman, Hofer and Schendel and McNamee.