CORPORATE PLANNING

Corporate Planning and Strategic Management

Corporate planning often ends with a hastily prepared business plan, prepared to satisfy debt or equity funding sources. While a plan prepared in such a way may meet it's immediate objectives, it is near worthless as a sound operations planning tool. What is real corporate planning and how is it done? A corporate planning process is described below. It is not the only viable method of corporate planning. But it does serve to outline the steps necessary to a good corporate plan. The key to success here, is not only the planning process, but also the successful implementation of the plan. It must be supported, monitored, and modified where necessary in order to be effective.

Phase I - Strategic Planning

The

Strategic planning phase begins the corporate planning process. This is the

planning phase in which all management come to an agreement as to the mission

statement of the company. Then more detailed strategic plans are created which

deal with market targets, product development issues and competitive issues.

Corporate strengths and weaknesses are discussed and plans are made to shore up

weaknesses and to continue to strengthen competitive strengths. The customer

receives a good bit of focus and definition during this phase as well. Once the

corporate strategic plan is complete, the department strategic planning can

begin. Department management can now work jointly to prepare their best

implementation of the corporate strategic plan within their own departments.

This planning process can work very rapidly into operations planning at the

department level.

Phase II - Operations Planning

This phase

begins with management setting objectives within their individual departments

which would ensure that the company can meet the strategic objectives set out

for the year. Then, with the assistance of a financial modeler, a corporate

operations plan is prepared which will integrate and orchestrate all of the

resources needed to meet the individual department objectives.

Phase III - Feedback and Control

No planning

is ever complete unless it puts measurable standards into effect, and then

compares those standards against actual performance and actively reviews and

manages the variances accordingly. Standards measurement includes budget to

actual expenditure comparisons on a monthly basis, milestone performance

measurements, market research results, questioning and interviewing.The below

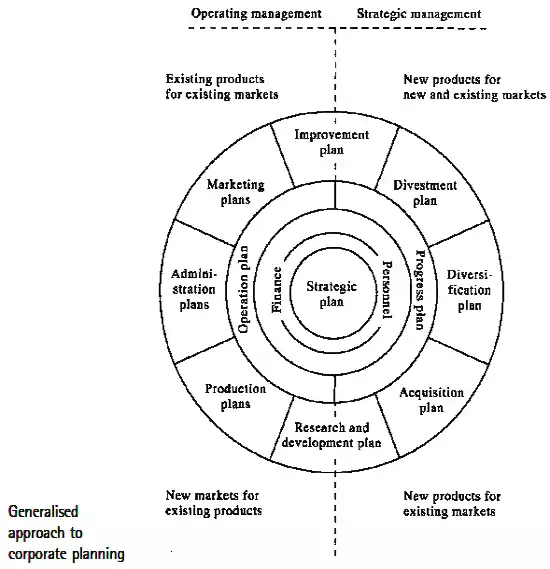

figure shows a generalised approach to a process of corporate planning.

Strategic management has divestment, diversification, and acquisition as three of its major components. Improvement, and research and development, are areas which may be either strategic or operating and are shown conceptually as coming under both (in reality it may be either) operating and strategic management.

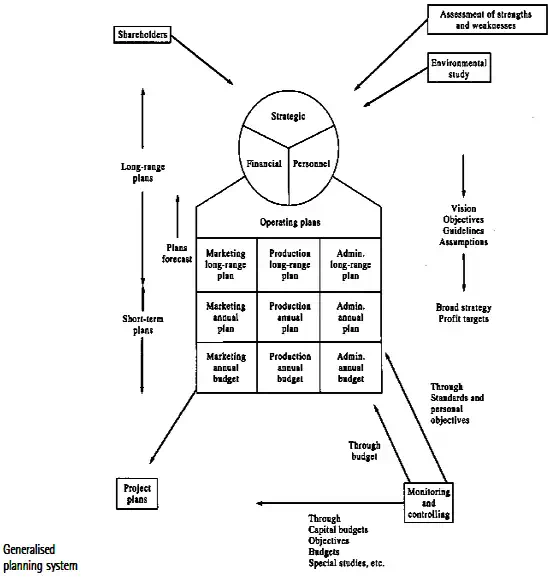

The above figure takes these concepts and turns them into a total planning system.The circle and the box on which it stands illustrate a simplified view of all the plans in the system, while the other boxes and arrows show stages in the planning system and information flows. Once again, the heart of the system is seen as the strategic, personnel, and finance plans. Strategy does not arise in a vacuum, and one of the first steps in planning is to perform an appraisal of strengths and weaknesses. This is likely to lead to a number of long- and short-term decisions, including many for profit improvement.

An immediate spin-off from this stage in the planning process might therefore be projects – symbolised by the box in the bottom left-hand corner. Most companies which practise strategic management try to achieve predetermined objectives which are related to the vision, and the process of setting these may be considered an integral part of strategic planning. Objectives are influenced by shareholders (although usually not explicitly) and, to some degree, by the assessment of strengths and weaknesses. The third key stage is to relate the company to its business environment. This has an effect on strategies through the identification of opportunities, the anticipation of threats, and the improvement of forecasts.

It may help the company to see where it has to take an avoidance action. From the total corporate strategy may be derived objectives and guidelines for the operating plans, and from the environmental study and its consideration in the strategic planning process may come defined planning assumptions. For a simple company, such as that shown in the diagram, the setting of objectives and targets may be easy. Most companies are much more complex, and the multidivisional, multinational organisation may find it a very complex matter. These problems receive more treatment later in the book, and a deeper consideration is given to what is meant by objectives.Long-range operating plans are properly the responsibility of those line managers in charge of the function or area concerned.

The diagram shows three functional areas: in practice there may be more, or the company may be organised into subsidiaries or divisions. Operating planning gives rise to plans and forecasts which flow back to the strategic planning process, where they are considered in the light of the company’s objectives and strategy, and may be either accepted or returned to operating managers for refinement. In turn, the considered plans of the operating units may lead to amendments to the thinking at strategic level and to changes in the strategic plans.

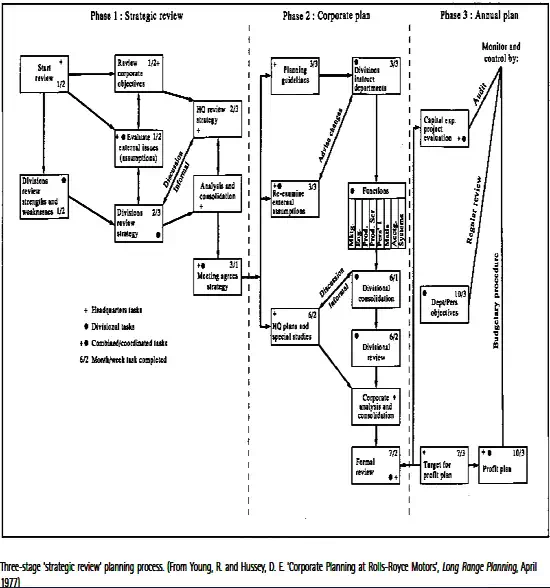

The strategic review process is designed to provide a forum for agreeing the main strategic issues and decisions in discussion between head office and business unit. Its input is a number of working documents at both levels, and a summary of the main strategic points as seen from each viewpoint. Its output is a set of agreed strategic guidelines which are then used as the framework for the detailed planning stage. The main advantage of the extra step is that it allows a free discussion and careful focus on the appropriate strategic issues, with major inputs from corporate level, before business units have become locked into their plans, and before the main issues have been swamped by the volume of the plan. It is easier to change before the plan has been completed than after, if only because the volume of work in completing a detailed plan can prevent easy alteration.

There are numerous other general systems which have been suggested from time to time, all of which have many similiarities with and some differences from the outline in the preceding pages.

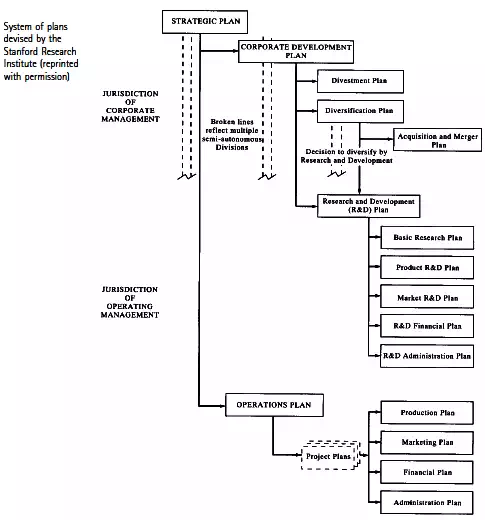

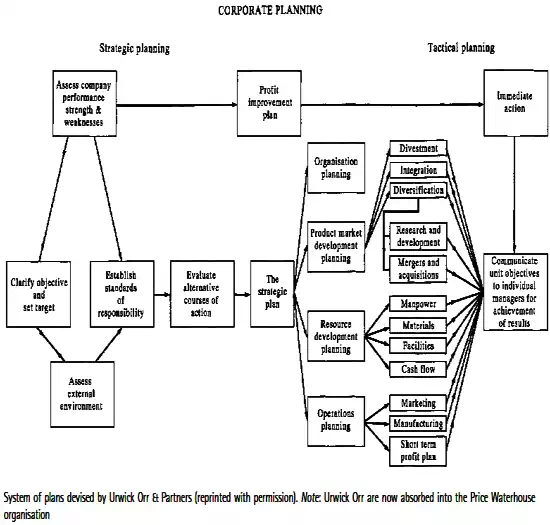

The above figure shows the system of plans suggested by the Stanford Research Institute. This, too, divides the planning task into two blocks. It divides the strategic planning task into a number of subunits. Basically, in the sense of this figure, the strategic plan shows the potential of the company and whether it can be attained from present operations. The development plan looks at the alternative ways in which the gap between potential and present operations may be filled, and moves through the two subplans for divestment and diversification. The second subplan again divides into acquisition and research and development. Although not specifically mentioned, it is possible to make provision for top level financial and manpower planning within the framework of this system.

An example of the derivation of policy and procedure from a plan may help to illustrate the relationships.

1. Plan. To reduce travelling expenditure of employees by 10 per cent in the following year by controlling class of travel, reducing frequency of travel, scrutinising expense claims more rigidly, and ensuring that all journeys are appropriately authorised.

2. Policy. All employees of the company are to travel second class on the railways unless the journey is of more than three hours (scheduled) duration.

3. Procedure. A defined system by which the policy is implemented and controlled – ticket-booking rules, expense claim forms and way of obtaining reimbursement, systems of authorisation of expense claims.

In any modern business there are hundreds of policies and procedures which must be applied if the organisation is to function at all. Definition provides a measure of uniformity, precision and control, and ensures that they are understood by all those who need to understand them. Where policies and procedures are of a ‘permanent’ nature they may beneficially be enshrined in books of regulations and standing orders. Every company has a host of these permanent areas: think for a moment of the areas of personnel, purchasing, office stationery, and general administration – although in many companies they are often implicitly rather than explicitly defined.

Careful attention to this area is a useful aid to better corporate planning. Often definition of a policy will lead to a recognition that it is incompatible with the plans and needs changing: if it is not defined it may be unknown to the people who would realise that it is inappropriate. The point should not be laboured, for there are no new principles involved, but it is nevertheless worth making.