One of the major aspects of preparing a correct financial statement is to distinguish revenue and capital in regard to revenue income, revenue expenditure, revenue payments, revenue profits, and revenue losses of the company with capital income, capital receipts, capital profit, or capital losses.

In fact, without differentiating, we cannot think of correctness of a financial statement. Ultimately, it will mislead the end results where no one can conclude anything. As per this principle, a revenue item should be recorded in the Trading and Profit & Loss account and a capital item should be recorded in the Balance-Sheet of respective firm.

Capital expenditure is the expenditure incurred to acquire fixed assets, capital leases, office equipment, computer equipment, software development, purchase of tangible and intangible assets, and such kind of any value addition in business with the purpose to enhance the income. However, to decide nature of the capital expenditure, we need to pay attention on −

· The expenditure, which benefit cannot be consumed or utilized in the same accounting period, should be treated as capital expenditure.

· Expenditure incurred to acquire Fixed Assets for the company.

· Expenditure incurred to acquire fixed assets, erection and installation charges, transportation of assets charges, and travelling expenses directly relates to the purchase fixed assets, are covered under capital expenditure.

· Capital addition to any fixed assets, which increases the life or efficiency of those assets for example, an addition to building.

Revenue expenditure is the expenditure incurred on the fixed assets for the ‘maintenance’ instead of increasing the earning capacity of the assets. Examples of some of the important revenue expenditures are as follows −

· Wages/Salary

· Freight inward & outward

· Administrative Expenditure

· Selling and distribution Expenditure

· Assets purchased for resale purpose

· Repairs and renewal expenditure which are necessary to keep Fixed Assets in good running and efficient conditions

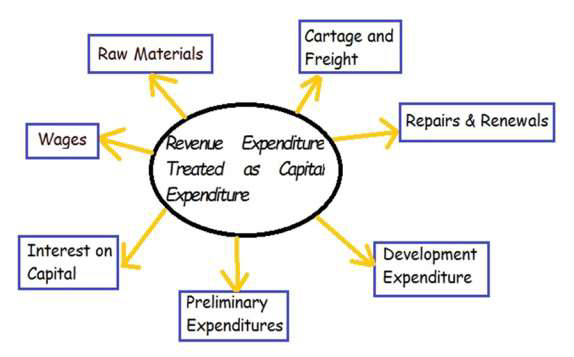

Following are the list of important revenue expenditures, but under certain circumstances, they are treated as a capital expenditure −

· Raw Material and Consumables − If those are used in making any fixed assets.

· Cartage and Freight − If those are incurred to bring Fixed Assets.

· Repairs & Renewals − If incurred to enhance life of the assets or efficiency of the assets.

· Preliminary Expenditures − Expenditure incurred during the formation of a business should be treated as capital expenditure.

· Interest on Capital − If paid for the construction work before the commencement of production or business.

· Development Expenditure − In some businesses, long period of development and heavy amount of investment are required before starting the production especially in a Tea or Rubber plantation. Usually, these expenditure should be treated as the capital expenditure.

· Wages − If paid to build up assets or for the erection and installation of Plant and Machinery.

Some non-recurring and special nature of expenditure for which heavy amount incurred and benefit for the same will spread in up-coming years, to be treated as capital expenditure and will be shown as the assets of the firm. Part of the expenditure should be debited to Profit & Loss account every year. For example, if heavy amount paid for the advertisement of a product, which benefits are expected to be received in next four years, then it should be debited as ¼ of the part in Profit & Loss account as the revenue expenses and balance ¾ will be shown as the assets in the Balance-Sheet.

The premium received on issue of shares, and the profit on sale of fixed assets are the major examples of capital profit and should not be treated as revenue profit. Capital profit should be transferred to the capital reserve account, which is used to set off capital losses in future if any.

Sale of fixed assets, capital employed or invested, and loans are the example of capital receipts. On the other hand, sale of stock, commission received, and interest on investment received are the main examples of revenue receipts. Revenue receipts will be credited to the profit and loss account and on the other hand, capital receipts will affect the Balance-sheet.

Discount on issue of shares and losses on sale of fixed assets are the capital loss and would be set off against the capital profits only. Revenue losses on normal business activity are part of the profit and loss account.