Secured Transactions And Creditors’ Rights

Businesses have relationships with banks, finance companies, and other businesses, both as lenders (creditors) and borrowers (debtors). Therefore, it is important to understand the rules of debt collection. This section begins by dealing with secured transactions and the rights of secured creditors to recover what is owed to them. It then discusses the rights of creditors in more general terms.

Secured Transactions

A security interest allows a creditor to seize specified assets of the debtor (usually referred to as collateral) if a debt is not repaid. Secured creditors do not need to bring a court action to enforce these rights. In contrast, unsecured creditors have to go through court and obtain a judgment against the debtor and an execution order authorizing seizure and sale of certain of the debtor's assets. Although acquiring security minimizes risk to the creditor, it may alienate customers; it is also more expensive and complex to acquire security. Typical transactions that involve security interests include vehicle, appliance, and furniture purchases on payment terms, and a bank or private lender providing a line of credit to a business that does not own real property. Security interests are regulated provincially for the most part under Personal Property Security Act (PPSA) legislation. Banks that are incorporated federally also have the option of federal regulation of security interests pursuant to the Bank Act.

How Security Interests are Created

Conditional Sales

In a conditional sale, title is not transferred to the buyer until he or she has completed a series of instalment payments. While the buyer has possession of the goods, the seller's retention of ownership provides full security since the seller may either sue for the unpaid balance, or repossess the goods and resell them. (An Ontario seller may then also sue for any deficiency between the amount owing and the sale price.) Ontario allows for an acceleration clause in a conditional sales contract, whereby the buyer must pay the whole balance owing upon default. An assignee of a seller under a conditional sales contract gets the same rights as the seller.

Assignment of Accounts Receivable

If accounts receivable are used as security for a loan, the bank can collect the assigned receivables owing to the business if the loan is not repaid. As long as the loan remains in good standing, the debtor is usually free to collect its own receivables and carry on business as usual.

General Security Agreement

The advantage of a general security agreement is that it gives a creditor the right to all of the debtor’s assets—both those in existence at the time of the agreement and those acquired after—if the debtor defaults on repayment. For the most part, general security agreements have replaced the floating charges that were used before modern PPSA legislation to give creditors first priority security interests in all personal property of debtors, not otherwise mortgaged or pledged, at the time of default under the loans secured by the floating charges.

Chattel Mortgages

While in a conditional sale, the security is represented by the very goods themselves, in a chattel mortgage, the debtor may give security over a variety of personal property, even property acquired after the chattel mortgage has been executed. A chattel mortgagee (bank) has remedies similar to those of a conditional seller. It can sue on the covenant to pay, take possession of the goods and resell them, and sue the mortgagor (debtor) for any deficiency. As long as the goods remain in the mortgagee’s possession, the mortgagor may redeem them by paying the balance of the debt with interest and costs.

Personal Property Security Legislation

PPS legislation was passed to try to reconcile the conflicting security interests in goods. It creates a single registration system for all secured interests, defines the secured parties, gives remedies against the debtor, and defines priorities among various secured parties and third-party purchasers or general creditors.

To create a valid security interest, the security interest must attach (both parties must have begun performing the agreement) and be perfected (either the secured party files a financing statement under the PPSA or takes possession of the collateral—the latter method is not common). A financing statement sets out the debtor, the secured party, and the general nature of the security interest.

Competing priority claims to the same asset are resolved by assigning priority to the creditor who first perfects its interest. If registration of a security interest is required (rules vary by province), failure to do so means third parties may acquire interests that prevail over the secured creditor, although their interests may not have priority over other claimants. Purchasers who fail to do a search under the PPSA may find that the seller did not have title to the goods, and the goods may be repossessed by the original owner.

Creditors' Rights

Often creditors, in the normal course of business, cannot afford the time or expense of securing debt against the property of the debtor. The remainder of this section outlines three statutory provisions intended to protect legitimate rights.

The Bankruptcy and Insolvency Act

A person is insolvent when he is unable to meet his debts to creditors as they fall due or when his liabilities exceed realizable assets. The federal Bankruptcy and Insolvency Act (BIA):

1. Establishes a uniform practice in bankruptcy proceedings throughout the country.

2. Provides for an equitable distribution of a debtor's assets among creditors.

3. Provides a framework for preserving and reorganizing the bankrupt's affairs by working out an arrangement with the creditors.

4. Releases an honest but unfortunate debtor and permits a fresh start.

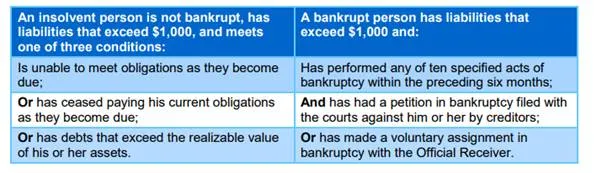

The Act distinguishes between potential candidates for bankruptcy (insolvents) and those who have declared bankruptcy (bankrupts). Insolvency “frequently precedes bankruptcy, but is only one of ten possible conditions that can help trigger bankruptcy. Figure provides further insights into the differences between being insolvent and bankrupt.

Figure : Insolvent v. Bankrupt.

A commercial business that finds itself in financial difficulty has a third option, and that is to file with the Official Receiver a notice of intention to make a proposal to its creditors. A proposal is a plan to restructure the business’s affairs for the purpose of enabling it to continue. Under the Companies' Creditors Arrangement Act, there is a similar means of avoiding liquidation by means of a compromise and arrangement. 169 The proposal requires approval of a majority of creditors (who are divided into classes with common interests) who constitute at least two-thirds of the value within that class. If approval is denied, there is a deemed assignment in bankruptcy by the debtor. If the creditors approve, the proposal must be approved by the court, which may withhold approval if the proposal is unreasonable, e.g., creditors are likely to get less than 50 cents on the dollar. Unless the proposal provides otherwise, the debtor retains control of its property, but payments are made to a trustee who distributes monies to the creditors.

Administration and Settlement of a Bankrupt's Affairs

A trustee in bankruptcy takes possession of the bankrupt's assets, although some assets (up to prescribed limits) are exempted for personal bankrupts (e.g., personal clothing, household furniture, motor vehicle). The trustee also takes possession of all books and documents relating to the bankrupt’s affairs. A stay of legal proceedings occurs, which means that creditors are not allowed to sue for payment of pre-bankruptcy debts, and all legal proceedings presently against the debtor are suspended.

Although the principal duties of a trustee are to recover all property that should form part of the debtor's estate and to apply that property in satisfaction of creditors' claims, the trustee has wide-ranging powers that also permit her to carry on the debtor’s business and to borrow money, etc., as long as she has the agreement of the inspector(s) appointed by the creditors to supervise her. Anything that happened up to one year before bankruptcy can come under scrutiny as to whether there was improper preferential treatment of certain creditors (fraudulent preferences). These can be unwound and become part of property for distribution to creditors generally. This is also the case for gifts of property made to the bankrupt before he or she became bankrupt (settlement) or non-arm's length transactions (reviewable transactions).

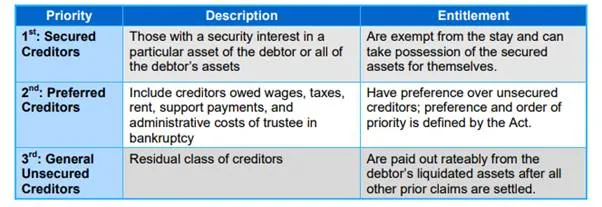

In paying out claims, the trustee must pay claims in proper priority, or he may be personally liable to the creditors. Figure identifies the priority among creditors.

Figure: Priority of Claims in Bankruptcy Proceedings

After the trustee has liquidated the debtor's assets and distributed the proceeds, the discharge of a bankrupt usually cancels the unpaid portion of debts remaining; the debtor has a clean slate and can start business again. A discharge is given at the court's discretion when it thinks that it is proper to do so. Reasons to refuse or suspend the discharge include payment of less than 50 cents on the dollar to unsecured creditors unless the debtor can't be held responsible under the circumstances, failure to keep proper books, continuing to trade once the debtor knew he was insolvent, causing bankruptcy by extravagant living, and being a bankrupt before. A bankrupt debtor who attempts to carry on business before a discharge is received must disclose that he is an undischarged bankrupt or be liable to criminal penalties.

Other Statutory Protection for Creditors

Bulk Sales A bulk sale is the sale of all, or essentially all, of the assets of a business. Ontario’s Bulk Sales Act (Ontario and Newfoundland and Labrador are the only provinces that have not repealed this legislation in view of comprehensive PPSA) establishes a procedure that makes it difficult for the owner of a business to dispose of stock-in-trade and business fixtures outside the normal business course without the payment or concurrence of trade creditors. The rationale behind such legislation is that if a debtor sells his stock-in-trade and business fixtures, the cash flow that creditors anticipated would arise from these assets (which formed the basis for extending credit in the first place) would be impaired. Application can be made to a court to exempt a bulk sale from the Bulk Sales Act.

Construction Liens (Mechanics' and Builders’ Liens)

Persons who have extended credit in the form of goods and services to improve land have a statutory right to record a security claim against the land that they have improved. If the claim of the lienholder is not paid, the lienholder may be able to cause the land to be sold and can receive payment from the sale proceeds.

A mechanics' lien is available, under most provincial acts, only to creditors who participate directly as workers or supply material for use directly in construction. The courts have held that an architect who prepares building plans is entitled to a lien. Ontario’s Construction Lien Act and some other provincial statutes entitle a lessor of equipment used in construction (but a seller of such machinery or tools is not entitled).

Registration of a mechanics' lien provides public notice of the lienholder's claim and establishes the lienholder's priority over unsecured creditors of the property’s owner, subsequent mortgagees, and subsequent purchasers. A lien that is not registered within the statutory time period (usually 90 days) ceases to exist. A principal contractor can achieve protection against the owner, but the Act also ensures that the principal contractor meets obligations to subcontractors.