Generally Accepted Auditing Standards (GAAS)

An independent auditor plan, conduct and reports the results of an audit under Generally Accepted Auditing Standards(GAAS) provide a measure of audit quality and the objectives to be achieved in an audit.

Auditing procedures differ from auditing standards. Auditing procedures are acts that the auditor performs during an audit to comply with auditing standards.

GAAS stands for Generally Accepted Auditing Standard. The most widely recognized auditing standards associated with the public accounting profession are known as generally accepted auditing standards.

10 GASS standards are approved and adopted by the membership of the AICPA, as amended by the AICPA Auditing Standards Board (ASB).

These are;

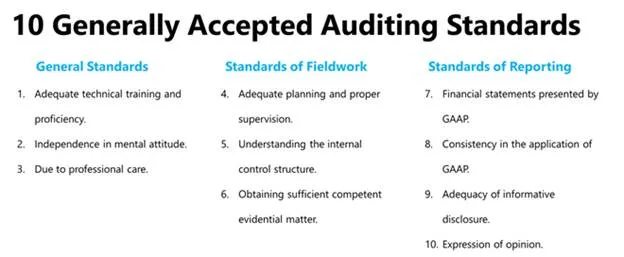

A. General Standards

B. Standards of Fieldwork

C. Standards of Reporting

· Financial statements presented by GAAP

· Consistency in the application of GAAP

· Adequacy of informative disclosure

· Expression of opinion

The three categories of the ten generally accepted auditing standards approved by the members of AICPA are explained below;

The general standards relating to the qualifications of the auditor and the quality of the auditor’s work.

In every profession, there is a premium on technical competence. The competency of the auditor is determined by three factors:

· Formal university education for entry in the profession,

· Practical training and experience in auditing, and

· Continuous professional education during the auditor’s professional career.

The auditor must be free of client influence in performing the audit and in reporting the findings. The auditor must also meet the independence requirements in the AICPA’s code of professional conduct.

The auditor is expected to be diligent and careful in performing an audit and issuing a report on the findings. The standard of due care requires the auditor to act in good faith and not to be negligent in an audit.

The fieldwork standards are so named because they pertain primarily to the conduct of the audit at the client’s place of business; that is, in the field.

The work is to be adequately planned, and assistants, if any, are to be properly supervised.

A sufficient understanding of internal control is to be obtained to plan an effective and efficient audit.

Sufficient competent evidential matter is to be obtained through inspection, observation, inquiries, and confirmations to afford a reasonable basis for an opinion regarding the financial statements under audit.

In reporting the results of the audit, the auditor must meet four reporting standards.

The first reporting standard requires the auditor to identify GAAP as established criteria used to evaluate management’s financial statement assertions.

The report shall identify those circumstances in which such principles have not been consistently observed in the current period in relation to the preceding period.

Informative disclosures in the financial statements are to be regarded as reasonably adequate unless otherwise stated in the report.

The final reporting standard requires the auditor to either express an opinion on the financial statements taken as a whole, or state that an opinion cannot be expressed.