Issue for Consideration other than Cash

In this case debentures are issued for consideration other than cash. Examples are allotment of debentures for assets purchased or technical services received. There is no receipt of cash in these transactions for the allotment of debentures. The following are the example of accounting entries:

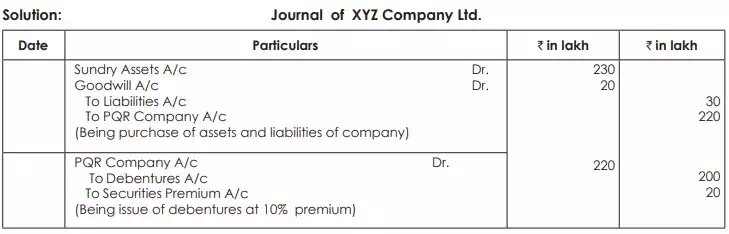

(For consideration other than cash).

The XYZ Company Ltd. took over assets of ` 230 Lakh and liabilities of ` 30 Lakh of PQR Company Ltd. for the purchase consideration of ` 220 Lakh. The XYZ Company Ltd. paid the purchase consideration issuing debentures of ` 100 each at 10% premium. Give journal entries in the books of the XYZ Company Ltd.