Credit Rating

In personal finance, the term credit rating commonly refers to a score issued by the Fair Isaac Corporation (a "FICO score"). A person's credit rating indicates how creditworthy he or she is.

In corporate finance, a credit rating is a "grade" assigned to a bond, bond issuer, insurance company, or other entity or security to indicate its riskiness.

How It Works (Example):

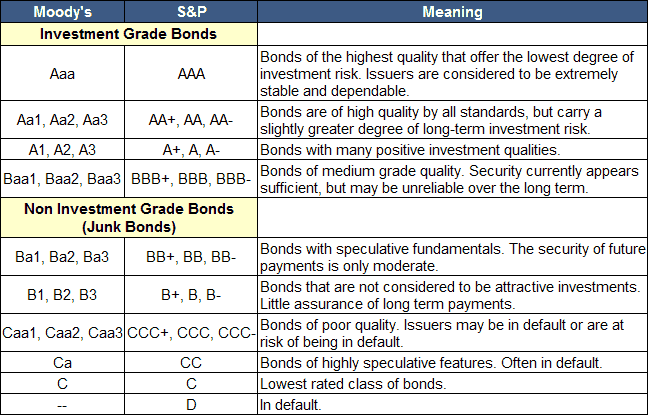

Bond rating agencies like Moody's and Standard & Poor's (S&P) provide a service to investors by grading fixed income securities based on current research. The rating system indicates the likelihood that the issuer will default either on interest or capital payments.

· For S&P, the ratings vary from AAA (the most secure) to C.

· For Moody's, the ratings go from Aaa to D which means the issuer is already in default.

Only bonds with a rating of BBB or better are considered "investment grade." BBB bonds are considered to be suitable for investment by institutions. Anything below the triple B rating is considered to be junk, or below investment grade. Bond ratings are periodically revised based on recent data.

Treasury Bonds are not rated because they are backed by the "full faith and credit" of the United States government. They are considered the safest of investments because the government has the power to levy taxes in order to pay its debts.

Why It Matters:

Credit ratings have huge influence on the price and demand for certain securities, particularly bonds: The lower the credit rating, the riskier the investment and the less the investment is worth. Therefore, lower-grade/higher-risk securities pay higher interest rates to attract buyers.

Low credit ratings are not always bad. They simply mean there is more risk associated with an investment and thus more potential for higher returns. In fact, many income investors actively enhance their returns by investing in lower-grade debt.