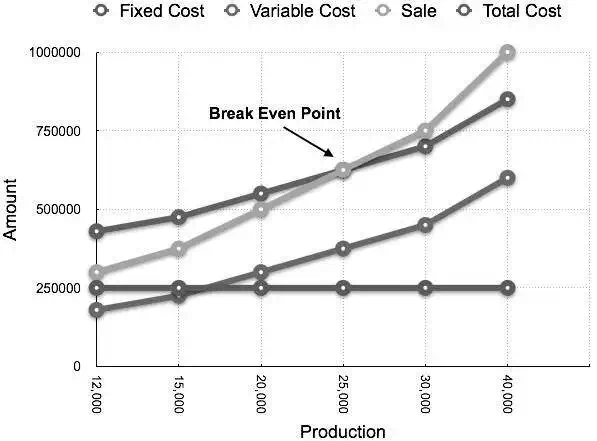

Break-Even Chart

Break-Even Chart is the most useful graphical representation of marginal costing. It converts accounting data to a useful readable report. Estimated profits, losses, and costs can be determined at different levels of production. Let us take an example.

Example

Calculate break-even point and draw the break-even chart from the following data:

Fixed Cost = Rs 2,50,000

Variable Cost = Rs 15 per unit

Selling Price = Rs 25 per unit

Production level in units 12,000, 15,000, 20,000, 25,000, 30,000, and 40,000.

Solution:

B.E.P =

Fixed CostContribution per unit

=

Rs 2,50,000Rs 10 × (Rs 25 - Rs 15)

= 25,000 units

At production level of 25,000 units, the total cost will be Rs 6,25,000.

(Calculated as (25000 × 14) + 2,50000)

|

Statement showing Profit & Margin of safety at different level of production Break Even Sale = Rs 6,25,000 (25,000 x 25) |

||||

|

Production (In Units) |

Total Sale (In Rs) |

Total Cost (In Rs) |

Profit (Sales - Cost) (In Rs) |

Margin of safety (Profit/Contribution per unit) (In Units) |

|

12000 |

3,00,000 |

4,30,000 |

-1,30,000 |

|

|

15000 |

3,75,000 |

4,75,000 |

-1,00,000 |

|

|

20000 |

5,00,000 |

5,50,000 |

-50,000 |

|

|

25000 |

6,25,000 |

6,25,000 |

(B.E.P) |

(B.E.P) |

|

30000 |

7,50,000 |

7,00,000 |

50,000 |

5,000 |

|

40000 |

10,00,000 |

8,50,000 |

1,50,000 |

15,000 |

The corresponding chart plotted as production against amount appears as follows: